Care Allowance 2026: How much money will be available in Germany?

Caring at home is a heartfelt but also demanding task. To ease your financial burden, there is care allowance. But how much are you actually entitled to, and how do you submit the application correctly? In this guide, you will learn everything about the current rates for 2026 and how to get the best support for yourself and your loved ones.

Care allowance is important financial support for you if you need help in everyday life due to illness or old age. If you care for yourself or a relative at home, care allowance can be valuable help in covering the costs of home care.

But the application and the exact requirements are not always easy to understand. You may be asking yourself: “How much care allowance will I get?” or “Who is actually entitled to it?” – these are the questions that concern many people in your situation.

In this comprehensive guide, you will learn everything worth knowing:

- Current amounts: The latest rates for the year 2026.

- Application process: How to get the decision step by step.

- Legal requirements: What must be fulfilled so that you are entitled.

- Combination options: How to cleverly combine care allowance with other benefits.

- Support for relatives: What help you can expect as a caregiving person.

We understand how challenging caring for a loved one can be. We want to make sure that you receive all the information you need to find the best possible support. Our goal is not only to provide you with facts, but also to give you the reassurance and confidence to make the right decisions for your situation.

Let us help you keep an overview and simplify the care process for you. Read on and find out everything you need to know now!

Before we dive deep into the details, imagine care allowance in Germany as an important foundation. It is more than just a simple transfer to your account – it is the tool that secures your self-determination within your own four walls. When everyday life becomes more difficult, this benefit ensures that care is not just a burden, but can take place on equal footing and with heart in a familiar environment.

Explanation of care allowance

Think of care allowance as financial backing that gives you the freedom to organize your care in the way that feels right for you. It is a direct cash benefit from long-term care insurance that is specifically intended for situations in which you are cared for in your own home.

The special thing about it: The money is not tied to rigid receipts. It serves as recognition and support so that you can, for example, financially compensate relatives, friends, or neighbors who lend you a hand in everyday life. So it is a kind of “support budget” that ensures valuable help in the familiar home is possible in the first place and appreciated.

Not everyone who needs help automatically receives care allowance. To ensure that support reaches those who need it most urgently, there are clear criteria:

1. The appropriate care level

In Germany, the basis for care allowance is classification into a so-called care level. Care allowance is paid from care level 2 onward.

- Care level 1: Unfortunately, there is not yet any direct care allowance here, because the impairments are still classified as less severe (however, you are entitled to other help here, such as the relief amount).

- Care levels 2 to 5: As soon as you are classified into one of these levels, you are fully entitled to the monthly payment. The higher your care level, the higher the amount, because, figuratively speaking, your need for support “grows” with it.

2. The type of care (home care)

A crucial point is who cares for you. Care allowance is intended so that you use self-arranged care assistance. This means:

- Family care: Your children, your partner, or other relatives take care of you.

- Volunteer help: Friends or acquaintances support you in everyday life.

- Important: If you hire only a professional care service, it bills the care fund directly via the so-called “care benefits in kind.” But you can combine both worlds (combination benefit), for example if you receive help from a professional and from your family.

Home care does not mean that you have to manage everything alone. You can use care allowance to find suitable caregivers or everyday helpers via platforms like noracares, who can step in exactly when your relatives need a break or support in the household is needed.

3. Care at home

The entitlement exists only if you actually live in your private environment – whether in your own apartment, in a house, or in a shared living arrangement. As soon as full inpatient care (nursing home) is used, a different financing system applies.

After benefits were gradually increased in recent years, 2026 offers a phase of stability. For you, this means: The amounts that were increased on January 1, 2025, will remain unchanged throughout the entire year 2026. This gives you a reliable basis for planning your everyday life and for the financial recognition of your caregivers.

Care allowance amounts by care level

So that you do not have to search for long, I have clearly compiled the monthly rates for the year 2026 here for you. The care fund transfers this amount to you monthly for your free use, provided that care at home is ensured by relatives or volunteers.

A little tip for you: If you also use a care service, the paid-out care allowance is reduced proportionally (this is called a combination benefit). It is worth calculating carefully here which mix fits your situation best.

Important differences between the care level stages

Classification into a care level is not just a matter of filling out forms – it reflects how much support you really need in daily life. The differences between the levels can be described vividly as follows:

- Care level 2 (Significant impairment): Imagine your everyday life starting to stall. You can still manage many things on your own, but you need support with personal hygiene or getting dressed. It is the level at which outside help becomes a regular support.

- Care level 3 (Severe impairment): Here the need for support becomes significantly more intensive. Perhaps walking becomes more difficult for you or you need help with daily nutrition. Independence is already greatly restricted here, and care takes a fixed place in your daily routine.

- Care level 4 (Most severe impairment): In this area, you depend on help almost around the clock. Whether with mobility within the apartment or coping with basic needs – without a helping hand, it is hardly possible anymore. The burden on caregiving relatives is particularly high here.

- Care level 5 (Most severe impairment with special requirements): This is the highest level. It is intended for people who need very specific and intensive care – often also at night or with medically complex requirements. The focus here is on maximum support to enable dignified care at home.

Submitting the application for care allowance feels like climbing a steep mountain for many people. But do not worry: You do not have to walk this path without a map. Basically, the application is the key that opens the door to the benefits you are entitled to. Above all, one thing is important: the right timing. Since care allowance is paid retroactively from the month of application, every single day counts, proverbially speaking.

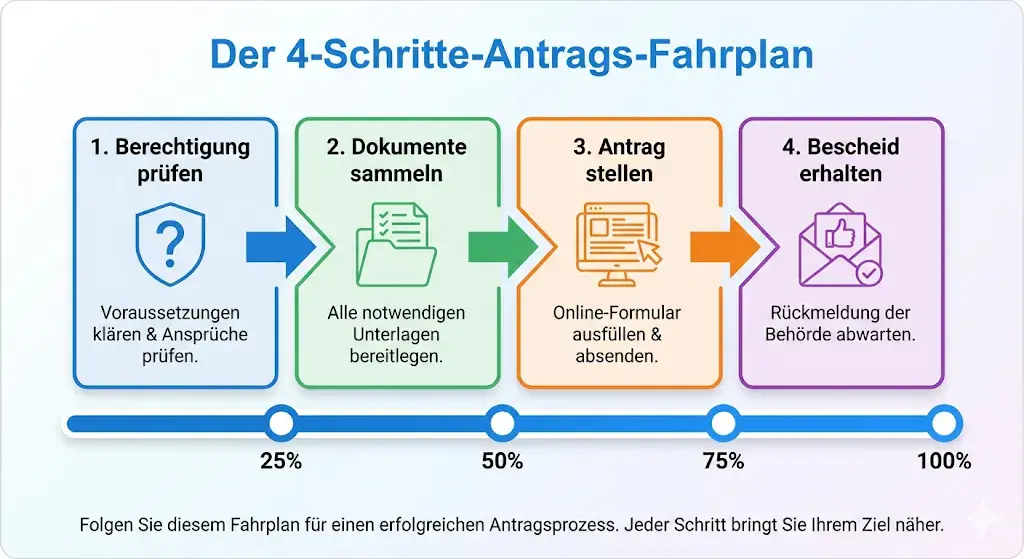

Step-by-step guide to applying for care allowance

The path to care allowance is not a sprint, but rather a well-planned hike. So that you do not stumble over bureaucratic roots, we will tackle the route together. If you follow these four steps, you will keep control at all times and make sure that no important document gets lost along the way.

Step 1: Determining eligibility (care level and care situation)

Before you fill out the forms, take a look at your daily situation. Do you already have a care level? If not, that is your first milestone. Ask yourself: Where exactly do you need help? Is it getting up in the morning, help with showering, or accompaniment to the doctor? If you expect at least care level 2 and your care at home is organized (for example by your family), you are ready for the next step.

Step 2: Collecting the required documents

Imagine that you are preparing a presentation of evidence. The care fund needs facts in order to assess your needs. Gather everything that documents your situation:

- Medical reports and current diagnoses from your general practitioner or specialist doctors.

- A list of medications, that you take regularly.

- Particularly helpful: A care diary. Note here over one to two weeks how much time your helpers need for which tasks. This is often the "gold standard" during the later assessment by the Medical Service (MD – formerly MDK).

Step 3: Submitting the application to the long-term care insurance fund

Now it becomes official. An informal phone call or a short letter to your long-term care insurance fund (which is affiliated with your health insurance provider) is enough to start: “I am submitting an application for long-term care insurance benefits.” The fund will then send you a detailed form. Fill it out calmly and explicitly tick “care allowance” if you organize the help through relatives.

Step 4: Follow-up and receipt of the benefit

After the application, the fund sends the Medical Service (MDK) to your home to assess you. As soon as the written notice lands in your mailbox and at least care level 2 is confirmed for you, the payment will be made. Keep an eye on your incoming mail and do not hesitate to politely follow up by phone after three to four weeks to ask about the status of the processing.

Common mistakes when applying and how to avoid them

To make sure your application goes through smoothly, you should know these typical pitfalls:

- Pretending to be “super strong”: Relatives often downplay the true burden out of exhaustion. To prevent things from getting that far in the first place, you can organize help early on. Through noracares, for example, you can find hourly support that has your back so you can fully focus on documenting your needs during the assessment.

- Sending the application too late: Care allowance is not paid retroactively, but only starting from the month in which the application was received. Do not wait for the perfect document—submit the application informally right away and send the documents later.

- Incomplete documentation: If you cannot say exactly how often you need help climbing stairs or eating, the assessor will estimate it—and often to your disadvantage. Be sure to keep a care diary so you can document your situation in black and white.

- Forgetting combination benefits: If you use a care service only for small tasks, you are still entitled to a proportional care allowance. Many people think “all or nothing,” but you can combine both to get the maximum out of it for yourself.

As soon as the care allowance reaches your account, the question arises: “Do I now have to keep every receipt?” The short answer is: No. The care allowance is a lump sum that is at your free disposal. It is your personal financial toolbox, with which you can put together exactly the help you need in your current stage of life. Whether you use it to reward your grandchildren for their driving service or to finance professional around-the-clock care is entirely up to you.

How care allowance can be used

Think of the care allowance as a budget for your quality of life. It is intended to ensure “self-procured care.” Since everyday life looks different for everyone, its use is wonderfully flexible:

- Recognition for relatives & friends: Most people use the money to give financial recognition to family members or friends who give their time and energy. It is a valuable compensation for their voluntary commitment.

- Professional support & 24-hour caregivers: You can use the money to pay for private caregivers or support persons (e.g. from Eastern Europe) who live with you and support you around the clock.

- Nursing home and inpatient costs: Even if you move into a nursing home, the principle of support remains—however, the form changes. While the classic care allowance is intended for home care, in the home the “benefit amount for inpatient care” is billed directly to the facility. Nevertheless, the care allowance can serve as a buffer for you during transitional phases or when financing additional services in the home.

- Aids and living comfort: Do you need a special senior bed that the insurance fund does not fully cover? Or would you like to treat yourself to a delivery service for healthy meals? Since the money is not earmarked for a specific purpose, you can also use it to make your living space more barrier-free or make everyday life easier with smart technology.

- Household help and garden: Sometimes it is not personal care that is difficult, but cleaning windows or mowing the lawn. Here too, you may use the care allowance to arrange helping hands for your home and yard.

Are there restrictions on how care allowance can be used?

Freedom in this case does not mean complete lack of rules. There are a few guardrails intended to ensure that you are still well cared for despite the financial freedom:

- The obligation to receive counseling: A care professional visits you for counseling. From 2026, the following applies uniformly to all care levels (2 to 5): proof once every six months is sufficient. The quarterly obligation for higher care levels has been abolished, but can still be used on request.

- Suspension of entitlement: If you have to stay in the hospital for a longer period or undergo rehabilitation, the fund will continue to pay the care allowance in full for the first eight weeks. After that, however, it is paused because full professional care during that time is already paid for by other providers.

- The intended purpose of “care”: Although you do not have to submit receipts, the fund assumes that the money is used to ensure your care. If, during a counseling visit, it is determined that care is being completely neglected even though the money is being paid, the fund can intervene and, for example, switch to benefits in kind (care service).

- Combination with benefits in kind: If you use an outpatient care service for basic care, the care allowance is reduced proportionally. You then receive only the percentage paid out that you have not already “used up” for the care service.

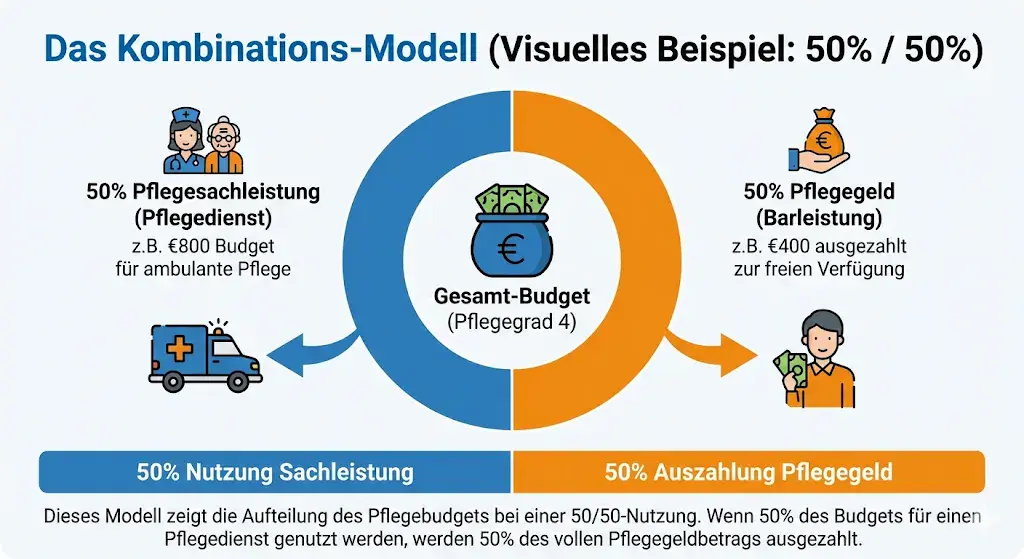

Caring for a loved one is rarely black and white. Often, help from the family alone is not enough, but a complete care service around the clock is also not desired. This is where the combination benefit comes into play. It is the “hybrid model” of long-term care insurance and offers you maximum flexibility to shape your everyday life exactly according to your needs.

What is a combination benefit?

The combination benefit allows you to combine care allowance (for your private helpers) with benefits in kind for care (for a professional care service).

The principle is simple: you use the care service for the tasks that your relatives cannot perform—for example, changing dressings properly or helping with the morning shower. The care service bills its costs directly to the long-term care insurance fund. If there is still some of your monthly budget for benefits in kind left at the end of the month, this remaining amount is converted proportionally into care allowance and paid out to you. This way, not a single cent of your entitlement is lost.

Example of combining care allowance and care benefits in kind

To make the whole thing more tangible for you, let’s look at a typical use case:

- The situation: You have care level 3. Your budget for benefits in kind (care service) in 2026 is a proud 1,432 euros. Pure care allowance would be 599 euros .

- The mix: You decide that a care service will come twice a week to help you with bathing. This professional help costs a total of 716 euros per month . That is exactly 50 percent of your available benefits-in-kind budget.

- The calculation: Since you have used only half of your benefits-in-kind budget, you are still entitled to 50 percent of the care allowance—50 percent of 599 euros = 299.50 euros.

- The result: You receive the professional help with bathing and an additional 299.50 euros in your account, which you can give to your daughter or son as recognition for the remaining care.

How to adjust your combination benefit

Life cannot always be planned rigidly. Maybe you feel better for a while, or your caring relatives need a vacation. Here is how you adjust your benefits:

- Use flexibility: You do not have to commit yourself to the long-term care insurance fund for years. The combination is automatically settled to the exact amount every month. If the care service uses more in one month (because you were ill, for example), your care allowance decreases. If it comes less often, your care allowance automatically increases.

- The 6-month choice: In principle, you are bound for six months to your decision about roughly how much benefits in kind you want to use. But do not worry: if your condition changes significantly, you can adjust this decision at any time with a short notice to the long-term care insurance fund.

- Submit a change request: If you notice that help from relatives is no longer sufficient in the long term, inform your care service. They often support you in increasing the scope of benefits in kind with the fund. A call to your long-term care insurance fund is usually enough to rebalance the ratio between cash and in-kind benefits.

When care remains within the family, that is often a great wish of everyone involved. It is an act of love and connection, but also an enormous physical and time burden. In Germany, the care allowance is intended exactly for this: it is not meant to relieve the state, but to enable you as a person in need of care to compensate your relatives for their valuable work. The money is, so to speak, the fuel that keeps the engine of home care running.

Can family members receive care allowance?

The short answer is: Yes, but indirectly. Legally speaking, the person in need of care is always the recipient of the care allowance. The money goes into your account. However, you have full freedom to pass this money on to your caring relatives (partner, children, siblings, or even grandchildren).

The nice thing about it: if you pass the care allowance on to your relatives as recognition for their care work, this amount is generally tax-free for your relatives. It is not counted as income as long as it does not exceed the amount of the respective care allowance. This way, the help arrives one-to-one where it is provided.

What are the responsibilities of family members?

Care allowance is not an “unconditional basic income.” It is tied to the expectation that care is provided professionally and with dignity. This results in important tasks for your relatives:

- Ensuring quality of care: Your relatives must ensure that you are adequately cared for – this ranges from personal hygiene and nutrition to mobility and support in everyday life.

- Participation in care consultations: As we have already learned, the regular visit of a care service (according to § 37.3 SGB XI) is mandatory. Your relatives should attend these appointments in order to receive tips and show the assessor that the care is running stably.

- Care diary and documentation: Even though there is no legal obligation to keep daily records as with a professional service, it is strongly recommended. If your condition worsens, your relatives can use it to provide complete proof of why a higher care level is necessary.

- Training: The care insurance fund offers free care courses. It is not a “hard” obligation, but the fund likes to see relatives make use of them to protect their own health (e.g. back-friendly lifting).

How family members can apply for care allowance

Since the care allowance is tied to the person in need of care, relatives often have to act as a “helping hand” with the bureaucracy. This is how you proceed together:

- Clarify authorization: So that your relatives are allowed to speak with the care insurance fund or sign applications on your behalf, a lasting power of attorney or a specific authorization to represent you before the health insurance fund is extremely helpful.

- Submit an application for a care level: The first step is always the application for classification (or reclassification to a higher level). Your relatives can submit this informally for you.

- Determine the payout method: In the official application form there is a field for the bank details. Here you can directly enter the account of the caring relative, if you want that. This way the money goes directly to where the work is being done.

- Administration and records: Your relatives should make sure that the appointments for the care consultations are arranged in good time. It is best to create a shared folder in which all notices from the care insurance fund and contacts with doctors are collected.

For many people, taxes and care allowance are a closed book. But the good news first: German tax law is surprisingly friendly here. Since care allowance is considered a social benefit, it is intended to benefit you and your helpers in full, without the tax authorities immediately taking a share.

How does care allowance affect taxes?

For you as a person in need of care, the matter is quite simple: The care allowance that you receive from the fund is completely tax-free. It does not count as income and does not have to be taxed in your tax return. It also does not reduce your other pension benefits.

It gets interesting when it is passed on to your helpers:

- For relatives: If you pass the money on to your family (or people with whom you have a close bond), it also remains tax-free for them. The tax office does not view this as salary, but as compensation for a “moral obligation.”

- Interaction with tax relief: The care allowance only slightly affects other deduction options. However, what is important is this: If you receive care allowance, you can only deduct the costs for an additional domestic helper or a care service from your taxes as a “household-related service” or an “extraordinary burden” if your actual expenses are higher than the care allowance received.

Additional financial support for caregivers

In addition to the monthly care allowance, there are other pots of money and tax tricks that support your relatives. A lot of real money is often left on the table here because people do not know the options:

1. The caregiver lump sum (the tax turbo for relatives)

Your caregiving relatives do an enormous amount. To compensate for that, there is the caregiver lump sum. This is a fixed amount that your caregiver can deduct in their own tax return – without having to present individual receipts for gasoline or cleaning supplies.

- For care level 2: 600 euros per year.

- For care level 3: 1,100 euros per year.

- For care levels 4 and 5: 1,800 euros per year.

This amount is available to your caregiver as long as they receive no payment for their help beyond the care allowance passed on to them.

2. The relief amount (€131 per month)

In addition to the care allowance, from care level 1 onward you are entitled to the relief amount of 131 euros per month. This money does not flow directly to your account as cash, but you can use it to pay for professional help, such as:

- A recognized domestic helper or shopping helper.

- Accompaniment services for walks or doctor visits.

- Day or night care. If the amount is not used in one month, it “accumulates” until June of the following year!

3. Pension and social insurance for your helpers

This may be the most valuable support: If your relatives care for you for at least 10 hours per week (spread over at least two days), the care insurance covers their pension insurance contributions. So your caregiver builds up pension entitlements while caring for you! Contributions to unemployment and accident insurance are also often covered by the fund.

Your path to care allowance – simple steps, clarity, and support! We know that caring for a loved one can be one of the most challenging tasks in life. Care allowance is meant to help make this task easier for you and provide the support you need so that you can focus on what matters most – the care and well-being of your relative or yourself.

With the information we have provided in this article, you now hopefully have a better understanding of how care allowance works, who is entitled to it, and how you can apply for it. Whether you are just dealing with the first steps or are already in the middle of the care process: it is important that you know how to make the best possible use of the financial resources and combine them cleverly with other support services.

Remember: care allowance is there for you to cover the costs of care – whether through the support of family members, 24-hour care, or the use of professional caregivers. Use the support you are entitled to!

If you still have questions or need help with the application, do not hesitate to contact your care insurance fund or a care advisor. Because you should feel safe and supported when it comes to organizing the right care for yourself or your relatives.

Now it is time to take the next step – apply for your care allowance and make use of the support you are entitled to!

- Care level – The official classification of individual care needs in Germany into five levels (1–5). From care level 2 onward, there is entitlement to monthly care allowance.

- Care insurance fund – The responsible provider of statutory long-term care insurance in Germany, which is affiliated with the respective health insurance fund and approves and pays out care benefits.

- Care benefits in kind – Professional care services that are billed directly between the outpatient care service and the care insurance fund – in contrast to care allowance, which is paid out in cash.

- Combined benefit – The possibility of using care allowance and care benefits in kind at the same time. The proportionately used benefits-in-kind budget is deducted from the care allowance; the rest is paid out in cash.

- Medical Service (MD) – The independent assessment body that carries out a home visit on behalf of the care insurance fund and officially determines the care level of the person in need of care.

- Relief amount – A monthly benefit of 131 euros granted from care level 1 onward and earmarked for recognized support services (e.g. domestic help, accompaniment services).

- Caregiver lump sum – A tax allowance for caregiving relatives that can be claimed in the tax return without individual proof (depending on care level, 600–1,800 euros/year).

- Respite care – Replacement care that steps in when the regular caregiver is temporarily unavailable (e.g. due to vacation or illness). The costs are covered by the care insurance fund.

- Care consultation visit (§ 37.3 SGB XI) – A legally required visit by a care service that checks the quality of home care. From 2026 onward, this must be documented once every six months.

- Lasting power of attorney – A legal document that allows a trusted person to act on behalf of the person in need of care – e.g. to submit applications to the care insurance fund or sign contracts.

- SGB XI (Social Code Book XI) – The German law on social long-term care insurance that regulates all benefits, rights, and obligations relating to care allowance and care insurance.